Can You use a Roth IRA to Save for College?

Education

|

Posted on February 15th, 2024

We usually like to start our blogs with a little more pizazz or maybe even an entertaining anecdote, but we don't want to be accused of doing the ol' bait and switch, so buckle up we're going straight into the weeds about the merits of saving for college with a 529 versus a Roth IRA. If that sounds like your cup of tea, you're in the right place.

We're comparing the two side by side to see which is the better option. Spoiler alert: it's a 529 plan. 529 plans and Roth IRAs both grow tax-free, but IRAs have some limitations when it comes to using them for college. As much as we wish there was a hack to college savings, a Roth IRA isn't it.

Financial Aid

Your expected family contribution (EFC) is the amount the federal government determines your family can reasonably spend on college tuition, and is calculated from the information entered in your Free Application for Federal Student Aid (FAFSA). Your EFC determines the amount and type of aid that a child will receive to attend college. This number can be affected by your assets, including savings and investment accounts.

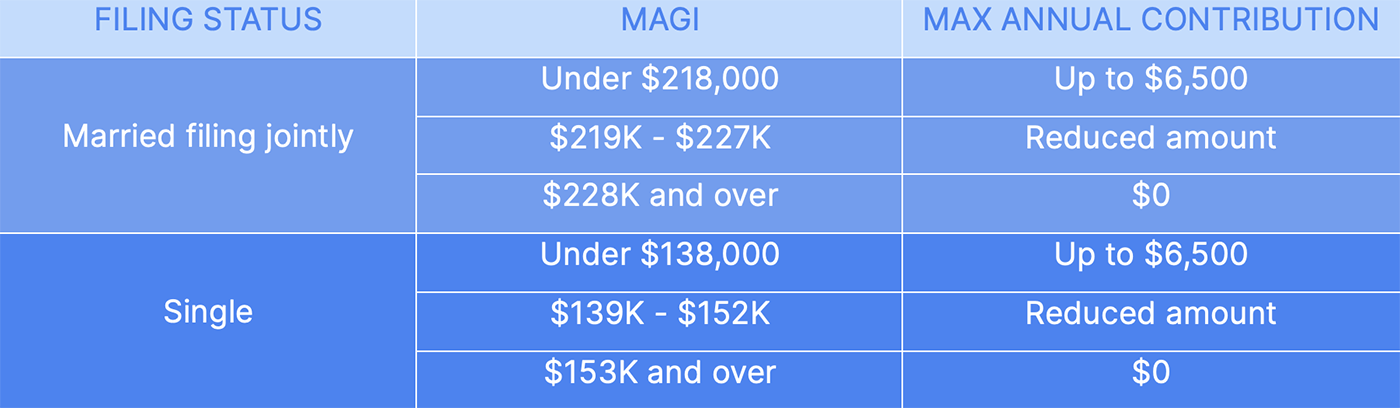

Income Limits

See how much you can contribute here:

This matters for two reasons. First, even if your MAGI is below the threshold now, if you expect to earn more than the contribution cutoff at some point, a Roth IRA will not be a good long term plan for college savings. Eventually you will lose the ability to contribute to this plan, and this can limit your ability to save enough to cover the cost of education. Second, you are only able to contribute $6,500 annually.

If you are planning on using this tax-advantaged account for your retirement as well, you likely won't be able to save enough to cover both.

There is also a gift feature, allowing a parent or grandparent to each contribute up to $15,000 ($30,000 for married couples) a year to a 529 plan while qualifying for gift tax exclusion. If you're one of the fortunate few, or you win the lottery, it is possible to superfund up to $75,000 ($150,000 for married couples) in one year to maximize your compounding returns, but then you can't touch the money for five years. The gift tax exclusion is for $15,000 per person, so you can still accept contributions from your aunts, uncles, friends, and more, even if a parent or grandparent or both have maxed out the gift tax exclusion for that year. Plus, most states tax deductions apply no matter what your income is. You can maximize your tax-advantaged accounts by using a 529 plan for college and a Roth IRA for retirement.

Penalties

Because these accounts are designed to help you save for a specific goal, there are penalties when they are used for other purposes.

If you have had the account under 5 years and are under 59 1/2, you will still have to pay the taxes when withdrawing funds for qualified situations, but you can avoid the 10% penalty. If the account is over 5 years old and you are making a withdrawal before you turn 59 1/2, you can avoid the taxes and the penalty. You can avoid either the penalty or the penalty and taxes (depending on the age of the account) in these situations:

- Qualified education expenses

- Unreimbursed medical bills

- Health insurance if you are unemployed

- First-time home purchase (up to $10,000 lifetime limit)

- Bills due to a disability

- Qualified childbirth or adoption expenses

When taking a distribution before you turn 59 1/2 it is crucial to confirm that any expense you plan to cover with the withdrawal is qualified. It is also useful to open the plan more than five years before you plan on using withdrawals to fund your child's education so you can avoid owing taxes.

If your child gets a scholarship, you can withdraw the amount equal to the scholarship without incurring the 10% penalty. You will still owe income taxes on the earnings, but never on the deposit. If for any other reason you don't need the money for college you can transfer the account to a new beneficiary without tax consequences.

Other Considerations

Will college become free? There are a lot of theories about changes in education policy over the next few years. 529 plans have changed over time inline with changing fiscal policy, and we expect that they'll keep doing the same. If college does become free, there will likely still be costs associated with education, such as textbooks, fees, room and board, meal plans, and other expenses to compensate for lost revenue from tuition.

It's also important to keep in mind that, if necessary, you can take out a loan to pay for college. You can't take out a loan for retirement.

It's important to protect your nest egg so when it comes time to retire, you are financially prepared to do so. Plus, your retirement fund can also benefit your kids. If you save effectively for your retirement, then it's less likely that your kids will have to support you in your old age.

No one else can contribute to your IRA, but you can get help from friends and family with a 529 plan.

(615) 517-2064 | 800 19th Ave S, 2nd Floor, Nashville, TN 37203

Raise Financial, LLC, a Tennessee Limited Liability Company, is an internet based investment advisory service. Our internet-based investment advisory services are designed to assist clients in personal investment and are not intended to provide comprehensive tax advice or financial planning. Our services are available to U.S. residents only. This website shall not be considered a solicitation or offering for any service or product to any person in any jurisdiction where such solicitation or offer would be unlawful.

Please consider your objectives and tax implications before investing with Raise Financial, LLC. All investments and securities involve risk. Raise Financial does not provide brokerage services.